Foreign Investment in U.S. Industry

The Labor Factor at the Core

Foreign direct investment (FDI) has long been a pillar of U.S. industrial growth, bringing capital, technology, and jobs. Yet in recent years, the enthusiasm of international investors has cooled. Concerns over regulation, tariffs, and national security scrutiny all play a role—but above all, the labor environment looms largest. High wage levels, chronic skill shortages, and uneven education pipelines are now as decisive as any policy measure in shaping foreign investment decisions.

Regulatory and Policy Frictions

International firms entering the U.S. quickly discover that regulation is a patchwork. Sales and use taxes vary by jurisdiction, environmental permits stretch timelines, and compliance costs pile up. Federal subsidies, designed to attract projects, can paradoxically increase costs by straining supply chains for construction materials and equipment. For foreign investors, the lack of predictability is often more damaging than the rules themselves.

Trade Policy and Tariff Pressures

Recent trade shifts—tariff hikes on raw materials, “Buy American” sourcing mandates, and remedy duties—have raised costs and reduced flexibility. For companies accustomed to global supply chains, being forced to buy U.S. inputs often means higher expenses and longer lead times. Projects that looked viable on paper before tariffs may no longer deliver acceptable returns.

The Central Challenge: Labor Costs and Talent Gaps

More than regulation or tariffs, it is the U.S. labor environment that shapes the viability of foreign manufacturing projects. The issues cut across cost, availability, and skills:

High wage levels. U.S. manufacturing workers earn far more than peers in Asia or Eastern Europe, immediately raising baseline operating costs. Rising wage pressures further complicate long-term projections.

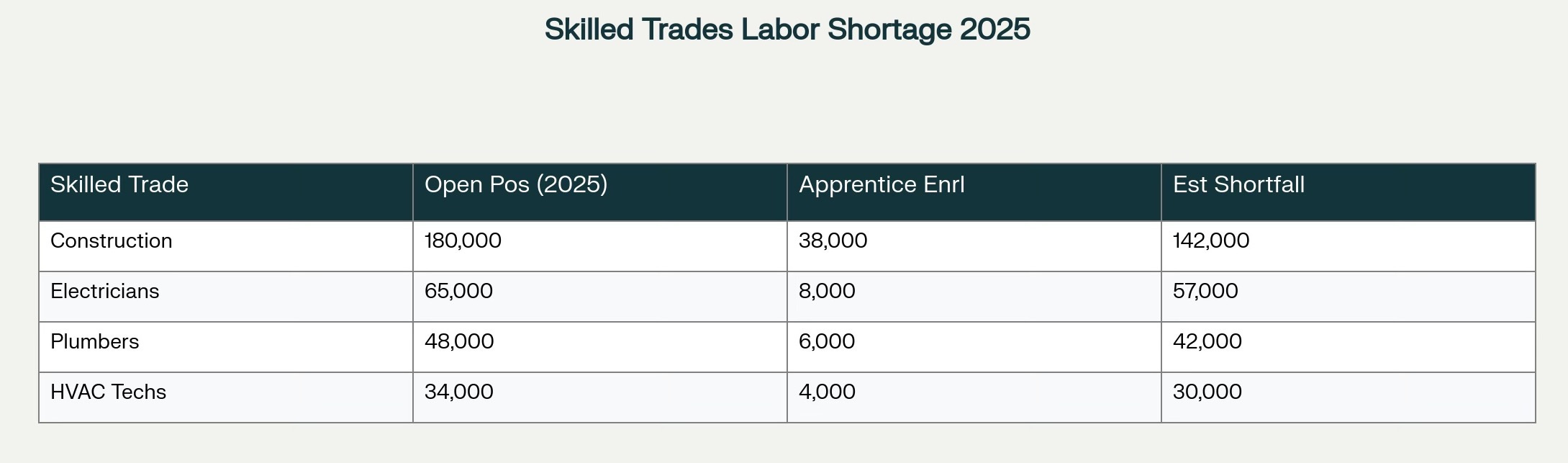

Scarcity of specialized skills. An estimated 1.9 million manufacturing roles could remain unfilled by 2033. Shortages are particularly acute in areas requiring technical expertise—robotics, precision machining, and advanced materials.

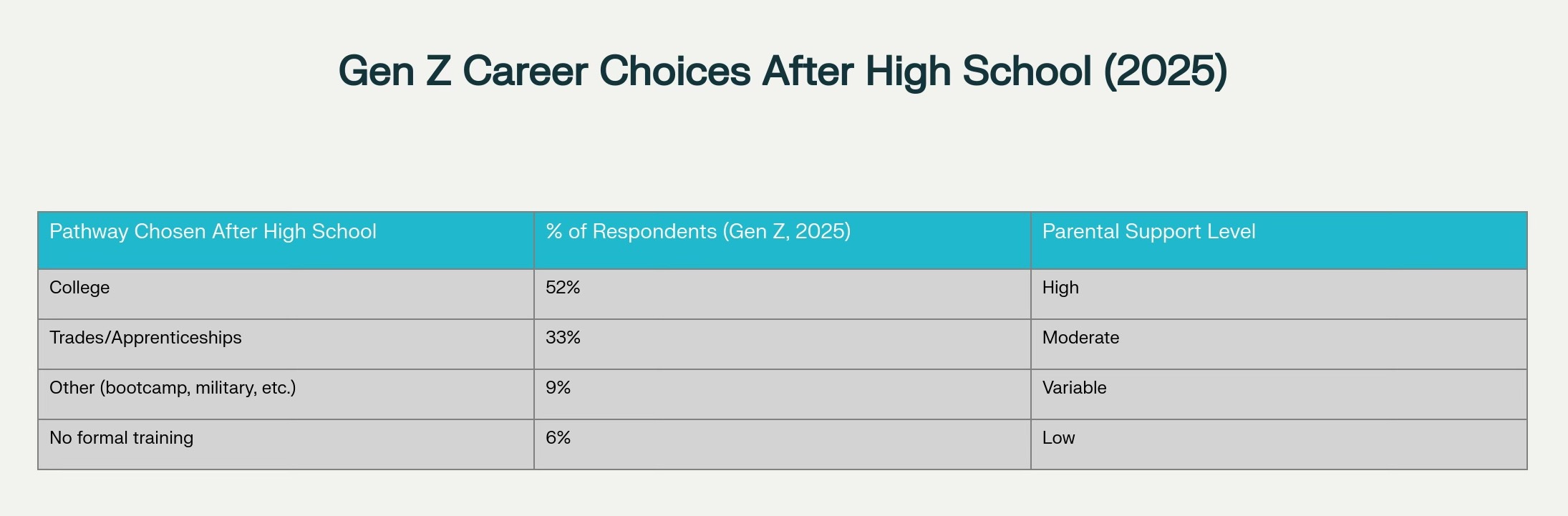

Education and training gaps. Many regions lack robust vocational pipelines. Under-resourced education systems leave companies to bear training costs themselves. This structural weakness forces investors to weigh whether they can realistically build a sustainable workforce.

Regional disparities. While states like Texas offer stronger talent pools and pro-business conditions, other regions lag behind, creating an uneven playing field across the U.S.

For foreign investors, labor is not just an operational cost item; it is a strategic risk. Without reliable talent pipelines, even well-financed projects can falter.

🔴 Labor & Skills

High wage levels

1.9M positions unfilled by 2033

Weak vocational/education pipelines

Regional disparities in workforce availability

Complex labor law & litigation risk

🟠 Regulation & Policy

Complex tax rules

Long environmental permits

Subsidy-driven supply bottlenecks

🟠 Trade & Tariffs

Tariff hikes on inputs

“Buy American” restrictions

Rising production costs

🟠 Geopolitics & Security

CFIUS unpredictability

Strategic sector restrictions

High-profile government interventionsLegal Complexity and Litigation Risk

Adding to the challenge is the structure of U.S. labor law. Firms must comply simultaneously with federal, state, and local rules. Employment litigation is common, and courts frequently award high damages. For executives accustomed to more centralized or less litigious labor markets, this unpredictability magnifies perceived risk.

Automation as a Partial Answer

To mitigate these labor constraints, many international manufacturers look to automation and digital technologies. Robotics, AI-driven production management, and advanced software can raise productivity and offset wage pressures. Yet this path demands capital-intensive investment and creates new needs for highly skilled technical staff—exactly the talent pool already in short supply. Automation, in other words, is a complement, not a cure.

Geopolitical and Security Scrutiny

Labor is the most consistent operational hurdle, but geopolitical oversight has become a growing barrier at the deal-making stage. The Committee on Foreign Investment in the United States (CFIUS) now exerts sweeping authority, particularly in sensitive sectors like energy, technology, and infrastructure. The government’s intervention in the Nippon Steel/U.S. Steel case underscored the political risks attached to cross-border deals. For investors, the fear is not only rejection but the reputational cost of failed transactions.

A Climate of Caution

The combined weight of these issues has slowed new investment announcements in conventional manufacturing. Many firms are pausing until there is greater clarity on tariffs, labor pipelines, and security approvals. Underlying all of these concerns is a growing doubt about whether U.S.-made products can remain globally competitive without continuous government support.

Conclusion: Labor at the Center of U.S. Investment Decisions

The U.S. remains a highly attractive market, with strong demand, advanced innovation, and legal protections. But foreign investors increasingly see labor—not just wages, but the entire ecosystem of skills, education, and law—as the defining variable for success.

Regulation, tariffs, and geopolitics shape the edges of the decision; labor determines the core.

Unless the U.S. strengthens its workforce pipelines through education reform, immigration policy, and vocational training, it risks discouraging the very capital it seeks to attract. For global investors, the calculation has become stark: America offers scale and opportunity, but only for those prepared to navigate a labor environment that is both high-cost and high-risk.